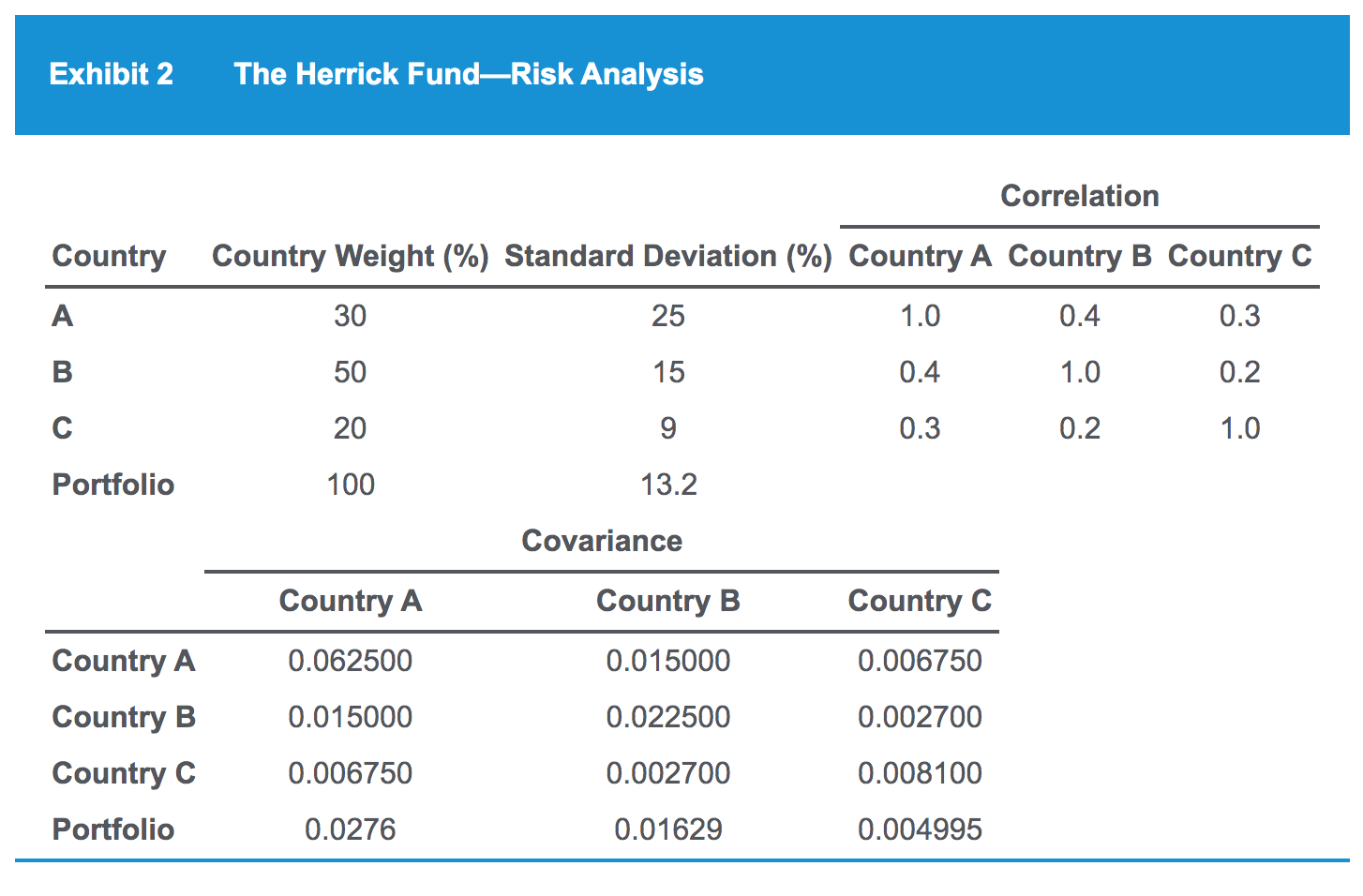

The Herrick Fund manager provides them with the information in Exhibit 2, which they use to carry out a risk attribution analysis.

Q: The proportion of the Herrick Fund’s portfolio variance contributed by Country A is closest to:

- 20.9%.

- 47.5%.

- 56.8%.

官网给的答案 B 47.5%,答案里的计算明明是错误的呀?请老师讲解一下正确的答案。多谢!