问题如下:

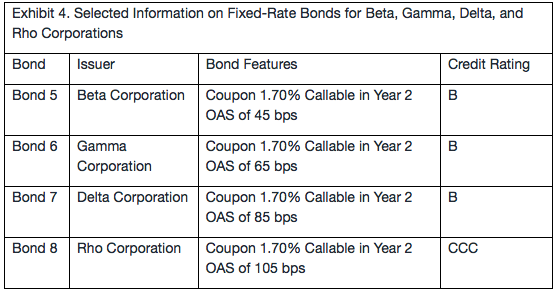

Carter asks Smith about the possibility of analyzing bonds that have lower credit ratings than the investment-grade Alpha bonds. Smith discusses four other corporate bonds with Carter. Exhibit 4 presents selected data on the four bonds.

Notes: All bonds have remaining maturities of three years. OAS stands for option-adjusted spread.

Which of the following conclusions regarding the bonds in Exhibit 4 is correct?

选项:

A. Bond 5 is relatively cheaper than Bond 6.

B. Bond 7 is relatively cheaper than Bond 6.

C. Bond 8 is relatively cheaper than Bond 7.

解释:

B is correct.

考点:考察对OAS的理解

解析:

Bond 5, Bond 6和Bond 7属于同一评级的债券 , 且其他特征 ( 如Coupon rate , maturity, callable data等 ) 相同 , 因此这两个债券属于可比债券 。 对于条件相似的含权债券 , 其OAS理论上应该相等 。 如果存在不相等的情况 , 较大的 ( OAS ) , 意味着该债券可能被低估 ( 便宜 ) 。

Bond 7 ( OAS 85 bps ) 比Bond 6 ( OAS 65 bps ) 更大 , 因此Bond 7相对更加便宜 。 因此B正确 , A错误 。

C不正确 , 因为债券8 ( CCC ) 的信用评级低于债券7 ( B ) , 单独的OAS不能用于相对价值比较 。 较大的OAS ( 105 bps ) 包含对B和CCC债券信用评级之间差异的补偿 。 因此 , 没有足够的信息来得出相对价值的结论 。

可是P134里面OAS 里面可以有credit risk啊?那如果credit不同有什么呢?