NO.PZ202208220100000205

问题如下:

Calculate the joint F-statistic and determine whether SMB and MOM together contribute to explaining RET in Model 3 at a 1% significance level (use a critical value of 4.849).

选项:

A.2.216, so SMB and MOM together do not contribute to explaining RET B.8.863, so SMB and MOM together do contribute to explaining RET C.9.454, so SMB and MOM together do contribute to explaining RET解释:

B is correct. To determine whether SMB and MOM together contribute to theexplanation of RET, at least one of the coefficients must be non-zero.

So, H0:bSMB = bMOM = 0 and Ha: bSMB ≠ 0 and/or bMOM ≠ 0.

We use the F-statistic, where

with q = 2 and n – k – 1 = 90 degrees of freedom. The test is one-tailed, right side,with α = 1%, so the critical F-value is 4.849.

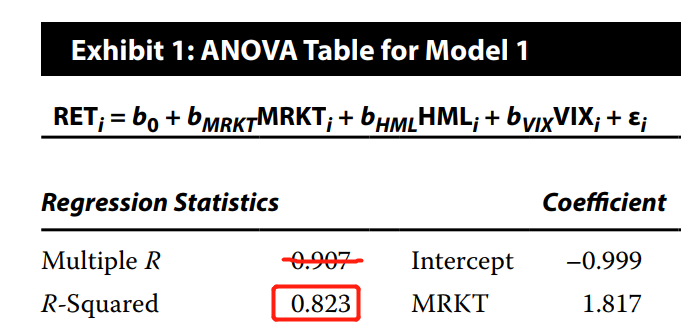

Model 1 does not include SMB and MOM, so it is the restricted model. Model3 includes all of the variables of Model 1 as well as SMB and MOM, so it is the unrestricted model.

Using data in Exhibit 1 and Exhibit 3, the joint F-statistic is calculated as

Since 8.863 > 4.849, we reject H0. Thus, SMB and MOM together do contribute to the explanation of RET in Model 3 at a 1% significance level.

[(0.9230-0.9070)/2]÷[(1-0.9230)/90]=9.3506 请问这个计算哪里错了?怎么结果不一样