问题如下:

7.Based on the mean-reverting level implied by the AR(1) model regression output in Exhibit 1, the forecasted oil price for September 2015 is most likely to be:

选项: less than $42.86.

equal to $42.86.

C.greater than $42.86.

解释:

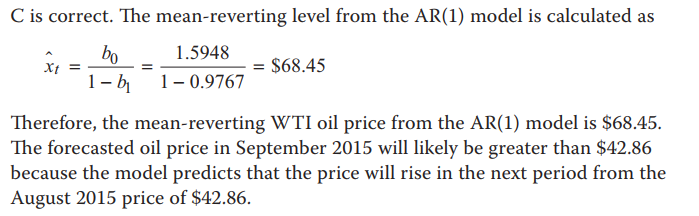

C is correct. The mean-reverting level from the AR(1) model is calculated as

[#PZMATH1348#]

Therefore, the mean-reverting WTI oil price from the AR(1) model is $68.45. The forecasted oil price in September 2015 will likely be greater than $42.86 because the model predicts that the price will rise in the next period from the August 2015 price of $42.86.

公式在哪里?公式在哪里?